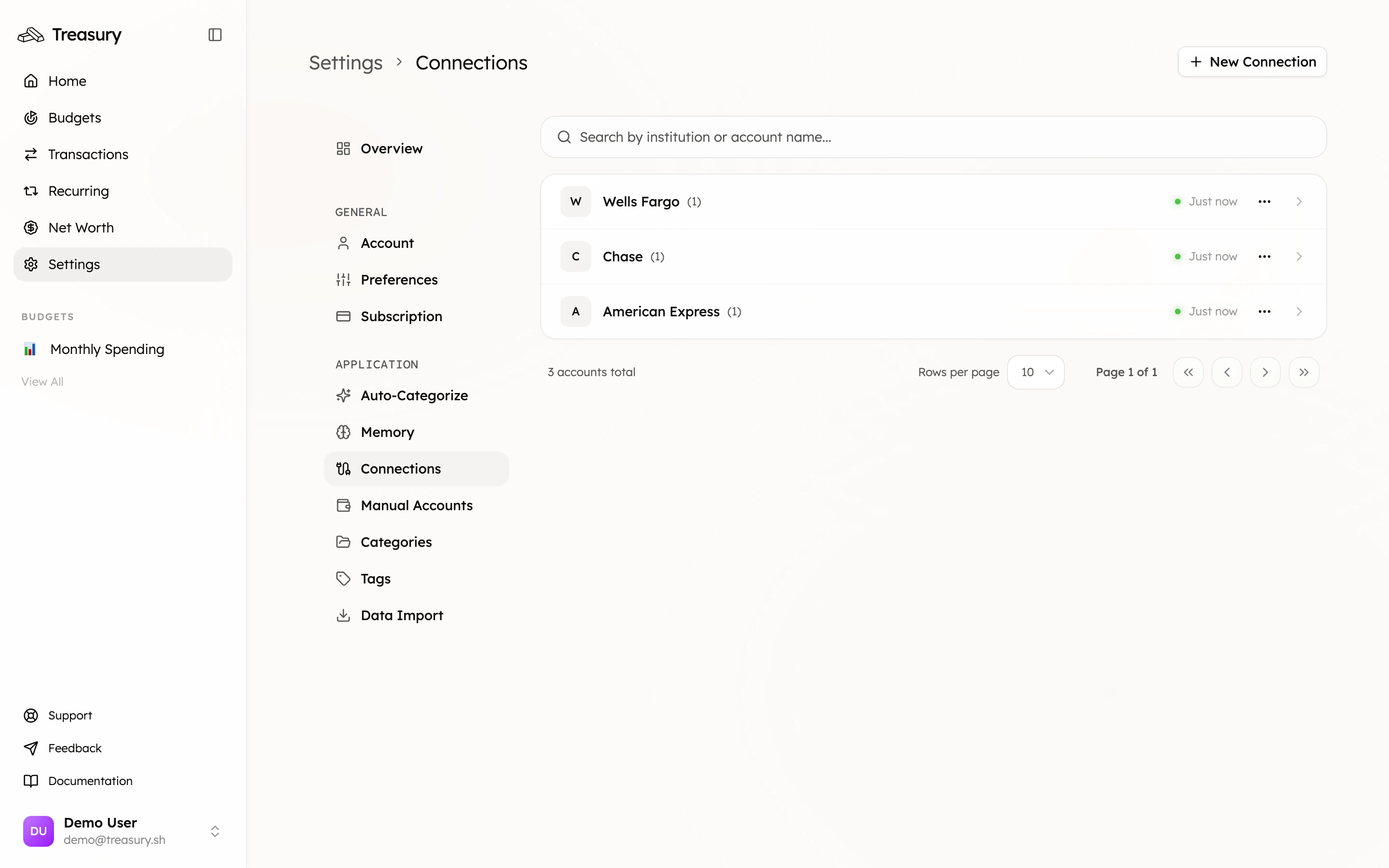

1. Connect what you can

Start by linking your banks, cards, loans, and investment accounts in Connections. These sync automatically, so their balances stay current without any effort.

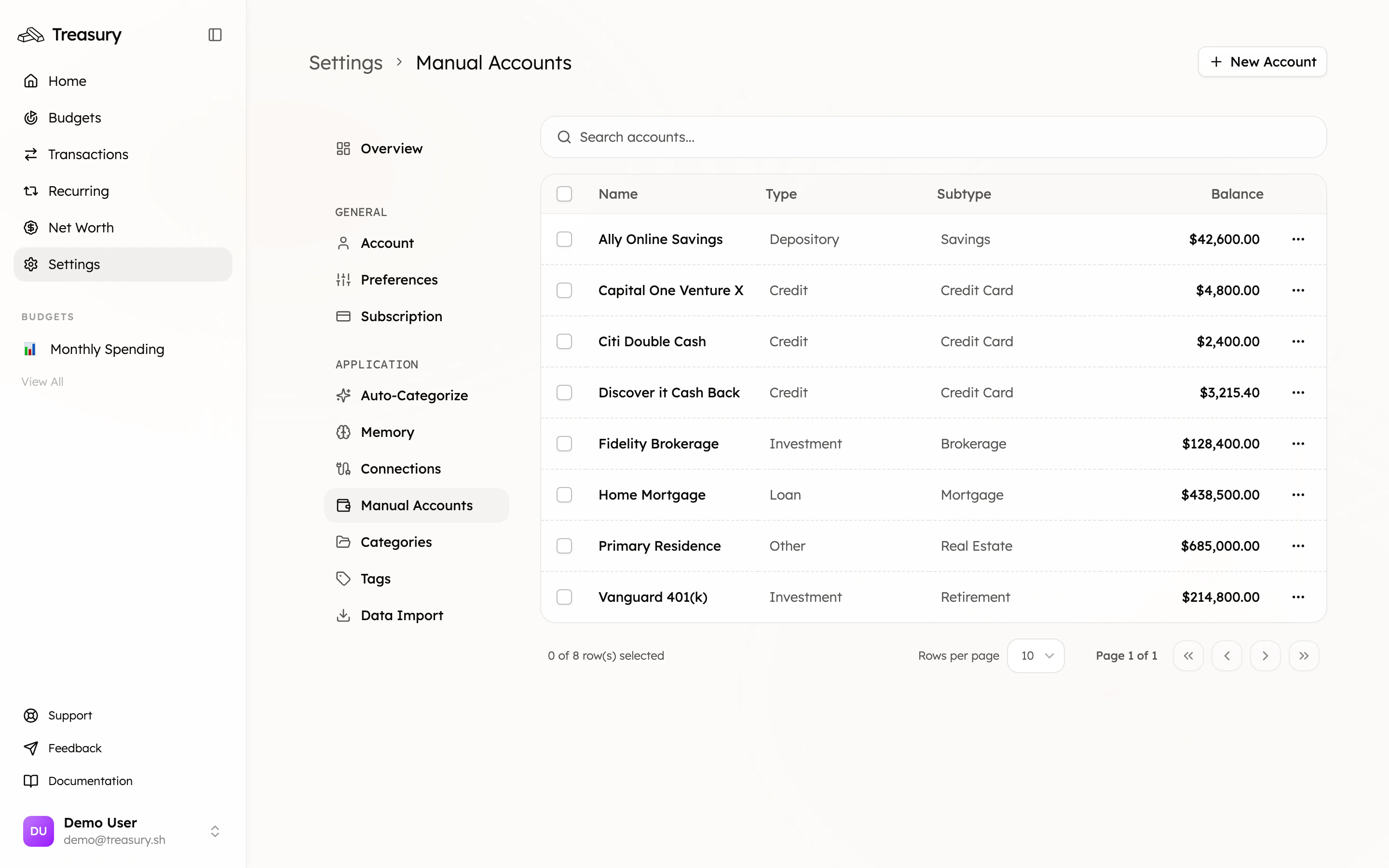

2. Add what you can’t

This is the step most people skip — and it’s the difference between a balance and a net worth. Add the big assets that don’t connect as manual accounts: your home’s estimated value, your car, cash, valuables, or an account at an unsupported institution.

3. Read your number

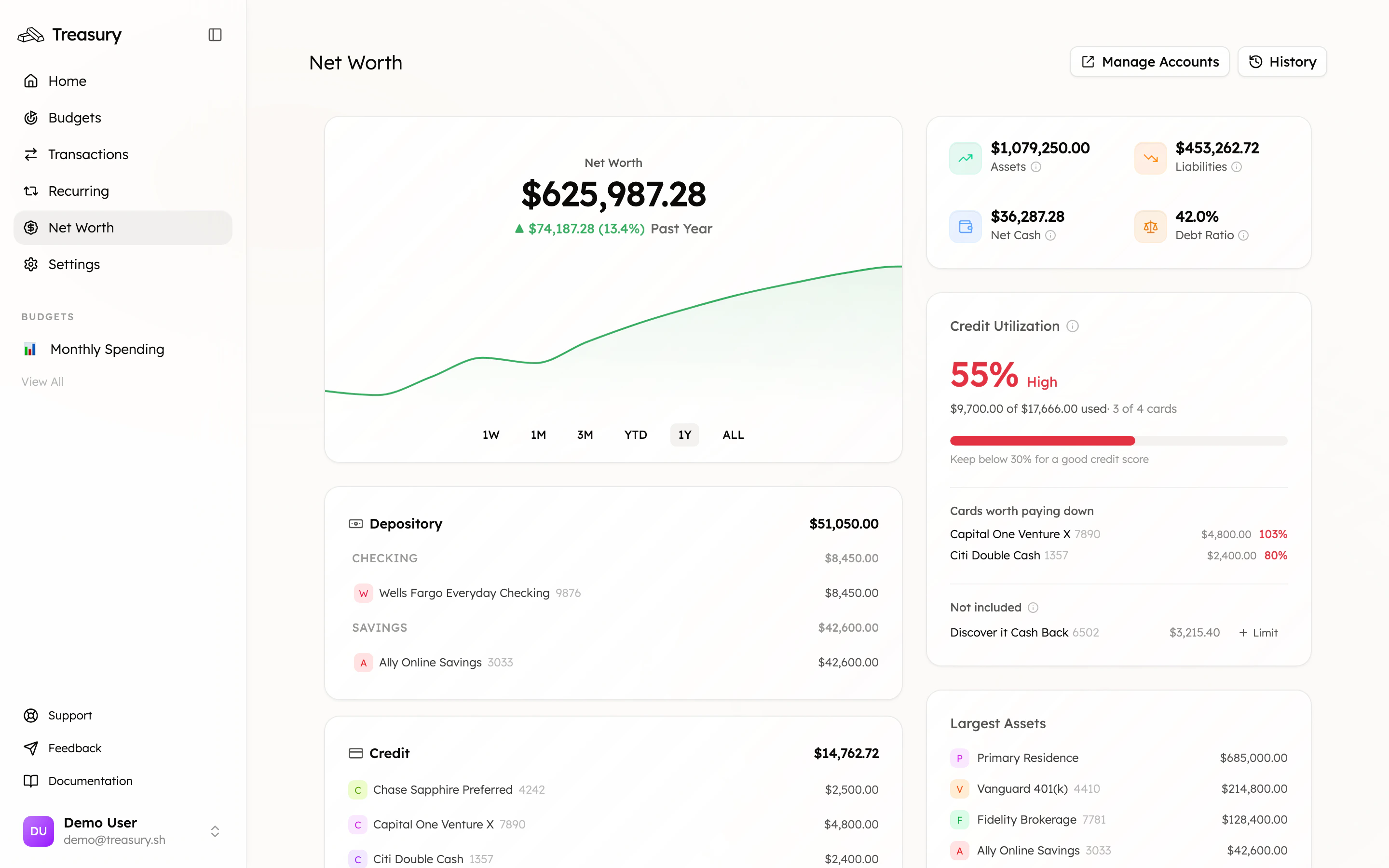

Open Net Worth. You’ll see assets, liabilities, and the bottom-line number — plus a trend you can view over any period.

4. Keep it honest

- Update manual values every month or two (home estimate, car value) so the number stays accurate.

- Reconnect promptly when a bank drops — a frozen balance skews the total.

- Mind utilization. The credit-utilization card flags cards worth paying down, which lifts net worth and your credit score.

What good looks like

A net worth that includes your home and car, not just your checking account — and a line that climbs over the year. That’s the number to watch.Take it further

Net Worth

The full feature reference.

Manual Accounts

Add and update what doesn’t sync.

Find & cancel subscriptions

Free up cash to grow the number.

Ask Treasury AI

“How has my net worth changed this year?”